By Brad Fedorchuk, VP, Group Marketing

We work in a big company, though it doesn’t always feel that way. Perhaps as a function of the often difficult to express “corporate culture,” we sometimes still see ourselves as a small prairie company. With a history that now spans over 125 years, it’s important to reflect on our sense of purpose. We provide coverage to more than nine million Canadians and 33,000 businesses, and it is crystal clear to me that my responsibilities extend beyond our company to the many Canadians who use our products.

|

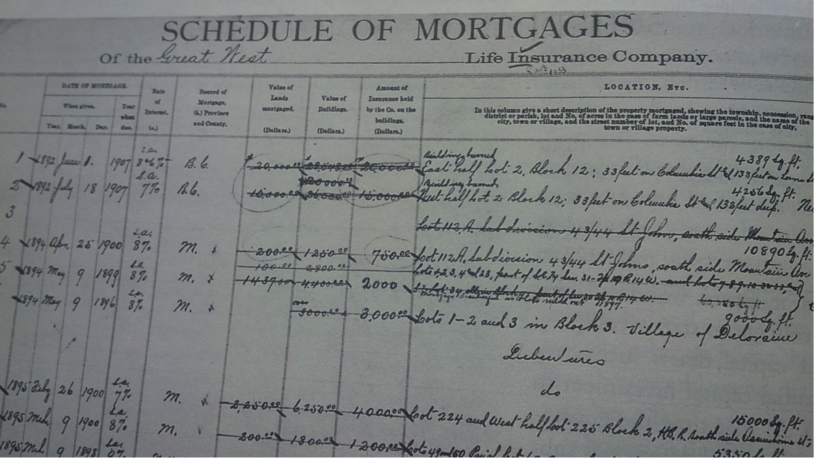

| How we tracked mortgages, once upon a time. |

Sometime between 1910 and 1920, a young, western Canadian farmer, Saskatchewan to be precise, found himself wanting to expand the family farm to meet the needs of his growing family. And, so it was, a mortgage was taken out with Great-West Life. Very appropriate since his needs were the very reason Great-West’s products were built.

That young farmer, as this story (perhaps predictably) goes, was my great-grandfather, James. I’m pretty sure James would be rather pleased that his great-grandson is now working for the company that saw and filled a need, and that our fundamental values haven’t changed.

|

|

Great-West was formed to help farmers in Western Canada.

|

Jumping forward about 100 years, we’re investing a lot of effort into health care. We’re researching and ensuring we manufacture products with clear purpose. Health care itself is highly inflationary, so I know we need to come up with product designs to help reduce costs. But, it’s health care, not cost care, so, with those same fundamentals, we’re filling a need by ensuring we pay the utmost attention to health needs. In short, we work to balance the health care needs of plan members with the affordability needs of plan sponsors.

This approach means a few things to our products:

- We take a long term view. As a multi-product carrier, it’s something we need to do. We know that certain drugs help patients avoid a disability, for example. So balancing today’s costs with longer term health benefits makes financial sense, and it makes sense for the well being of our plan members.

- We go beyond paying a claim. If someone were at risk of drowning, you would throw him a life line? For sure, and you’d stick around until you were satisfied he was safe. If we see that plan members aren’t compliant with their health treatment, we increasingly challenge ourselves to identify those situations and offer support. Paying a claim is a necessary part of what we do, but it’s not always sufficient in helping plan members achieve better health.

- We do our best to avoid hard rules. We’re all different; we have different DNA, different habits and different capabilities when it comes to managing health. It’s easier to implement rigid rules than to recognize these differences. But, where we can, we try to offer exception processes and case management processes. In exchange, we ask plan members to try lowest cost services where they can.

|

| We seek to offer products that leave no Canadian behind |

Will our products sell better or be more profitable with this approach? To be honest, I’m not sure, but I do know that no matter what our approach, not every customer will choose our products. I hope that those who do choose our products, will be aligned with our sense of purpose and fundamental values.